An integrated 360° perspective on Financial Crime controls and regulation starts from the premise that effective Financial Crime risk management cannot be understood through the lens of a single function, procedure, control, regulatory framework or line of defence. Financial Crime risk typically arises, develops and materialises in the space between commercial decision-making, client onboarding, transaction processing, tax assessment, legal interpretation, compliance monitoring, internal escalation, audit testing and management accountability. A client seeking genuine control over Financial Crime risk therefore does not need an isolated review of policy documents, an abstract legal memorandum or a technical control review detached from operational reality. The client needs a coherent perspective that reveals how risks actually arise, how signals move through the organisation, where decisions are made, where exceptions are permitted, where controls intervene, where evidence is created and where formal compliance may diverge from actual control. Hands-on experience across the first line of the business, the second line of tax, legal and compliance, and the third line of audit provides an exceptionally strong foundation in this regard, because it shows how the same Financial Crime risk may carry a different meaning, urgency and decision logic within different functions.

Such a perspective brings Financial Crime Risk Management back to its core: the decisive question is not whether rules, policies or control descriptions exist, but whether the organisation as a whole is capable of identifying risks in time, assessing them carefully, managing them proportionately, escalating them consistently, documenting them demonstrably and subjecting them to critical review. Integrated Financial Crime Risk Management therefore requires an approach in which regulation, governance, operations, monitoring and assurance do not exist alongside each other, but reinforce each other. The strength of a 360° view lies in the fact that the client not only sees what has formally been put in place, but also understands how the system functions under pressure: in situations involving commercial tension, time pressure, complex clients, cross-border structures, unclear ownership arrangements, tax sensitivities, sanctions risks, unusual transactions, data gaps, requests for exceptions and regulatory scrutiny. From that broad practical experience emerges a sharper, more realistic and more controllable picture of Financial Crime control: one that does not stop at paper-based assurance, but supports the client in building a sustainable, effective and testable Integrated Financial Crime Risk Management model.

Practical experience across the first, second and third lines as the basis for integrated integrity management

Practical experience across the first, second and third lines forms the basis for integrated integrity management because Financial Crime risk is perceived, assessed and addressed differently in each line. The first line often experiences Financial Crime risk at the intersection of client contact, commercial objectives, operational timelines and day-to-day decision-making. That is where the first encounter occurs with client behaviour, transactions, documentation, explanations, requests for exceptions and commercial interests. The second line translates that same risk into normative frameworks, policy requirements, legal boundaries, tax considerations, compliance standards and regulatory expectations. The third line then assesses whether the overall framework of governance, policies, controls, execution, monitoring and remediation has been designed with sufficient reliability and operates in a demonstrable manner. Without experience across all these positions, the view of Financial Crime risk management inevitably remains partial. An assessment from the first line alone may remain too operational. An assessment from compliance alone may become too normative. An assessment from audit alone may lean too heavily on testability after the event. The added value arises where these perspectives are brought together into one integrated form of integrity management.

Within Integrated Financial Crime Risk Management, this line-transcending practical experience is of particular significance because it prevents responsibilities from appearing formally clear while actual cooperation remains insufficiently robust. In many organisations, there is a clear division on paper between risk ownership, standard-setting, monitoring and assurance, yet concrete files reveal that decision-making becomes fragmented. The business may assume that compliance will provide direction; compliance may expect the business to provide complete signals; legal may focus on legal defensibility; tax may assess fiscal qualifications; and audit may later conclude that the file lacked sufficient coherence. The issue is then not necessarily that individual functions have acted negligently, but that the overall system does not operate in an adequately integrated manner. Practical experience across the lines makes visible where these handover points are vulnerable, where responsibilities become blurred, where information is lost and where decisions are not recorded with sufficient precision. This creates a stronger foundation for integrity management that does not depend on isolated interventions, but on coherent operation.

For the client, this means that Integrated Financial Crime Risk Management is not approached as an abstract organisational model, but as a practically controllable system in which people, processes, systems, controls, escalations and testing must connect with one another. The value of hands-on experience across the three lines lies in the ability to assess whether the first line truly understands the risks it owns, whether the second line provides sufficiently directional and executable standards, and whether the third line delivers assurance that offers substantive insight into operation and vulnerability. That perspective strengthens the quality of management decisions, because recommendations are not only legally defensible, but also operationally applicable, controllable and explainable to regulators, auditors and stakeholders. Integrated integrity management thereby becomes concrete: responsibilities are sharpened, handover points are designed more deliberately, escalations are assessed more consistently and controls are positioned where they actually reduce risk.

Insight into how Financial Crime risks manifest differently across the lines of defence

Financial Crime risk does not manifest uniformly within an organisation. In the first line, it often appears as client behaviour that raises questions, a transaction that deviates from the expected pattern, a structure that appears commercially attractive but raises integrity concerns, or a documentation flow that is incomplete, inconsistent or difficult to verify. For the business, the risk is usually directly connected to client service, revenue, speed, relationship management and operational feasibility. As a result, a signal in the first line may be experienced as a disruption to the process, while the same signal may constitute, from a compliance or legal perspective, a material indication of increased Financial Crime risk. That tension makes line-specific insight necessary. A view limited to the formal control description misses how risk is framed, normalised or deferred in commercial practice. A view limited to the legal standard misses how execution pressure, client expectations and system constraints affect the effectiveness of that standard.

In the second line, Financial Crime risk assumes a different form. There, the risk is not primarily seen as a client file or operational deviation, but as a matter of interpretation of standards, policy consistency, risk tolerance, tax and legal qualification, sanctions law, anti-money laundering obligations, corruption risk, fraud prevention, monitoring logic and regulatory expectations. The second line must be able to convert signals from the business into clear frameworks and executable requirements, but in doing so it also runs the risk of becoming too detached from day-to-day practice. A policy may be substantively strong while still failing to align sufficiently with the systems, data, capacity and decision moments with which the first line operates. A legal or compliance assessment may also be substantively correct, but provide insufficient direction as to what concrete action is now expected from the business. Insight into this second-line dynamic is essential, because Financial Crime control is not strengthened by more complex standards alone; it is strengthened when standards are translated into lines of conduct, decision rules, evidentiary requirements and escalation criteria that can be applied in practice.

In the third line, Financial Crime risk manifests differently once again. Audit looks at design, existence, operating effectiveness, consistency, evidentiary quality and management follow-up. It becomes visible there whether the organisation not only has policies and controls, but can also demonstrate that they actually function. The third line exposes where files are insufficiently substantiated, where monitoring outcomes are not followed up, where exceptions become structural, where management information is insufficiently reliable and where governance appears stronger on paper than in practice. This third-line perspective is indispensable within Integrated Financial Crime Risk Management, because it forces the organisation to look beyond intention and design towards demonstrable operation. For the client, combining these three manifestations produces a much sharper risk picture: Financial Crime risk is not reduced to a compliance issue, but made visible as a chain risk that simultaneously touches commercial choices, legal interpretation, tax assessment, operational execution and assurance.

Understanding the tension between commercial objectives, risk management and assurance

One of the most defining features of Financial Crime risk management is the permanent tension between commercial objectives, risk management and assurance. Commercial organisations pursue growth, client retention, market access, speed and competitive strength. Financial Crime controls, by contrast, require care, verification, documentation, monitoring, escalation and sometimes delay or rejection. Assurance then requires decisions to be testable, consistent and defensible after the event. These three forces are not naturally in balance. In concrete files, commercial urgency may place pressure on client due diligence, risk management may be perceived as an obstacle to business, and audit may later identify shortcomings that were insufficiently visible or insufficiently taken seriously during execution. A strong Integrated Financial Crime Risk Management model recognises this tension not as an incident, but as a structural reality that must be carefully governed.

This tension becomes particularly visible with complex clients, cross-border structures, transactions with an increased risk profile, tax uncertainties, sanctions-sensitive jurisdictions, intermediaries, beneficial ownership issues, unusual payment flows and files in which reputational risk, legal risk and commercial value intersect. The business may wish to retain a relationship because it is strategically important. Compliance may require additional information because the risk profile has not been adequately explained. Legal may point to contractual or liability risks. Tax may raise concerns relating to fiscal substance, transfer pricing, withholding taxes or transparency issues. Audit may later assess whether the decision-making process was sufficiently traceable. Without a clear understanding of this tension, a pattern can easily arise in which each function acts from within its own mandate, while the overall decision is not robust enough. Integrated Financial Crime Risk Management must therefore provide for clear risk tolerance, explicit decision-making criteria, timely escalation, documented balancing of interests and testable record-keeping.

For the client, this understanding has significant practical value because it prevents Financial Crime control from being presented as a choice between commercial strength and compliance. Effective control does not mean that commercial objectives are ignored; it means that commercial decision-making is strengthened by risk awareness, legal clarity, tax precision, compliance discipline and assurance value. A well-designed approach makes visible which risks are acceptable, which mitigating measures are required, which exceptions require management approval and which files do not fit within the risk appetite. Assurance thereby ceases to be an after-the-event mechanism that merely exposes shortcomings and instead becomes an integrated source of quality improvement. The client consequently gains a decision-making model in which commercial interests are not detached from integrity, but are assessed within a framework that remains defensible to regulators, shareholders, clients and internal stakeholders.

Experience in translating regulation into policies, processes and control activities

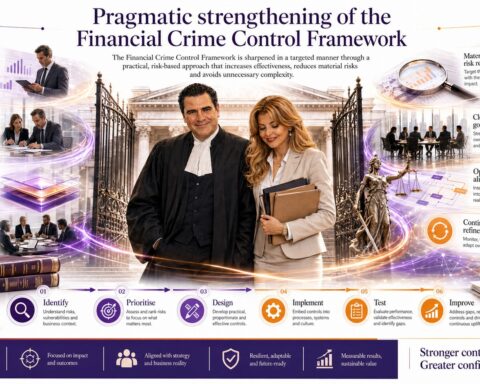

Financial Crime regulation only acquires practical value when it is translated into policies, processes and control activities that genuinely guide conduct. Laws and regulations in the areas of anti-money laundering, sanctions, corruption, fraud, tax integrity, client due diligence, transaction monitoring, reporting obligations and governance are complex, layered and continuously evolving. A legal analysis of these standards is necessary, but insufficient where translation into daily operations is missing. The organisation must know what information must be collected during client onboarding, which risk factors trigger enhanced due diligence, which transactions require escalation, which functions are responsible for assessment, what documentation is required, which systems generate signals, which controls take place periodically and how deviations are followed up. The core of Integrated Financial Crime Risk Management therefore lies in the translation from standard to operation.

This translation requires experience with both regulation and execution. A policy document may be legally complete, yet operationally deficient if it does not make sufficiently concrete how employees are expected to act. A process description may appear logical, yet fail where data are unavailable, systems are not connected, roles are insufficiently clear or exceptions remain outside the field of vision. A control may be correctly designed, yet insufficiently reduce risk where it takes place too late in the process, depends on incomplete information or mainly produces administrative confirmation. Experience in converting regulation into policies, processes and controls makes it possible to identify these weaknesses at an early stage. The point is not to stack additional layers of control, but to design measures that are proportionate, aligned with the risk profile and demonstrably contribute to control.

For the client, this means that Integrated Financial Crime Risk Management is made concrete and executable. Regulation is translated into clear policy standards, workable procedures, practical decision trees, risk-based client segmentation, effective control points, clear escalation mechanisms, relevant management information and testable file-building. This approach makes it possible to treat compliance not as a separate legal obligation, but as an integrated component of business operations. The client receives more than an interpretation of standards: a workable control model emerges in which legal requirements, tax considerations, operational processes, compliance monitoring and audit expectations connect with one another. The ultimate added value lies in the ability to convert rules into conduct, conduct into evidence, evidence into insight and insight into controllable improvement.

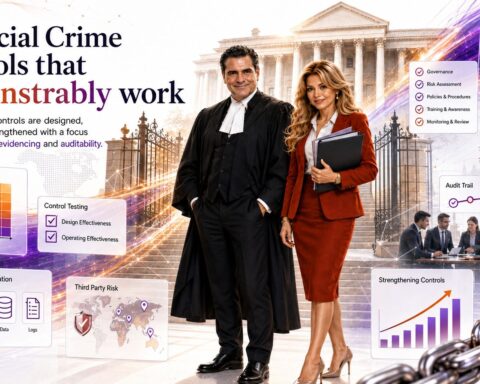

Insight into where controls are effective in practice and where they mainly provide false assurance

An essential component of a 360° perspective on Financial Crime controls is the ability to distinguish between controls that actually reduce risk and controls that mainly suggest formal assurance. Many organisations have extensive control frameworks consisting of checklists, four-eyes principles, periodic reviews, system alerts, approval steps, reports and audit trails. Their presence may create the impression that Financial Crime risk is adequately controlled. Yet practice often shows that certain controls mainly confirm that a process step has been completed, without any substantive assessment of whether the underlying risk has been adequately understood. A tick-box can show that documentation is present, but not that the documentation is reliable. A review can show that a file has been examined, but not that the reviewer has been sufficiently critical. An alert can show that a system generated a signal, but not that the subsequent analysis was substantively sound.

False assurance often arises when controls are designed from the standpoint of formal compliance rather than risk effectiveness. A control that is formulated too broadly, takes place too late in the process, contains no clear assessment criteria, depends on incomplete data or is performed routinely without substantive challenge contributes only limitedly to actual control. Within Financial Crime Risk Management, this risk is significant because many controls relate to complex, context-dependent and interpretative risks. The question whether a transaction flow is unusual, whether a structure has sufficient economic rationale, whether a client explanation is credible or whether a tax route raises integrity concerns cannot always be reduced to a simple checklist. Integrated Financial Crime Risk Management therefore requires controls that not only exist, but are also substantively sharp: focused on relevant risk indicators, supported by reliable information, performed by competent and authorised employees, and underpinned by clear escalation and documentation requirements.

For the client, this insight is particularly important because it helps prevent resources from being spent on controls that mainly create administrative burden without meaningful risk reduction. A strong assessment makes visible which controls can be simplified, which controls must be strengthened, where duplications exist, where blind spots arise and where additional monitoring is needed. This involves looking at design, operation, timing, ownership, evidentiary value and alignment with regulatory expectations. Effective controls are reinforced and embedded more firmly. Controls that mainly provide false assurance are revised, replaced or removed. As a result, a stronger Integrated Financial Crime Risk Management model emerges in which control activities are not assessed by volume, but by relevance, depth, operation and demonstrable contribution to control.

Connecting business, tax, legal, compliance and audit in one coherent perspective

Connecting business, tax, legal, compliance and audit in one coherent perspective is a core prerequisite for effective Integrated Financial Crime Risk Management, because Financial Crime risks rarely remain within the boundaries of a single discipline. A client structure may be commercially attractive, fiscally complex, legally permissible, compliance-sensitive from an elevated risk perspective and difficult to test from an audit standpoint. A transaction may fit the client profile from a business perspective, yet require further interpretation from a sanctions, money laundering, fraud or corruption risk perspective. A tax planning arrangement may remain within the boundaries of technical regulation, yet still raise integrity concerns due to a lack of economic substance, opaque ownership arrangements or the use of high-risk jurisdictions. A contractual structure may be legally defensible, yet provide insufficient operational visibility into the source of funds, involved intermediaries, ultimate beneficial owners or payment flows. Financial Crime control therefore requires a multidisciplinary perspective in which each function retains its own sharpness, but decision-making does not fragment into separate partial assessments that insufficiently connect with one another.

A coherent perspective means that the business is not viewed solely as a commercial executor, tax not solely as a fiscal specialist, legal not solely as a legal gatekeeper, compliance not solely as a guardian of standards, and audit not solely as an ex post testing function. Each discipline has its own information position and its own form of risk understanding. The business sees client behaviour, commercial intent, market pressure and operational specificities. Tax sees fiscal structures, substance issues, cross-border money flows and possible indicators of abuse or avoidance structures. Legal sees contractual risks, liability, authority, sanctions clauses, reporting obligations and legal defensibility. Compliance sees normative consistency, client integrity risks, transaction monitoring, policy adherence and regulatory expectations. Audit sees evidentiary quality, control operation, governance, follow-up and structural deficiencies. Integrated Financial Crime Risk Management brings these information positions together, so that the overall risk picture does not remain dependent on coincidental handover, individual alertness or separate escalation channels.

For the client, this connection materially strengthens managerial control. When business, tax, legal, compliance and audit are placed within one coherent perspective, a decision-making model emerges in which commercial feasibility, fiscal interpretation, legal sustainability, compliance risk and auditability are weighed simultaneously. This prevents risks from becoming visible only after an incident has occurred, a regulator raises questions or audit concludes after the fact that the substantiation is insufficient. An integrated approach makes it possible to determine at an early stage which files require multidisciplinary assessment, which signals must be interpreted jointly, what minimum information must be available and which decisions must be recorded at management level. As a result, the client does not receive a fragmented control framework, but a coherent steering mechanism in which functions reinforce one another, blind spots are reduced and Financial Crime risks are managed with greater precision, proportionality and evidentiary value.

Understanding how escalations, exceptions and incidents move through the lines

Escalations, exceptions and incidents are the moments within Financial Crime control where the difference becomes visible between a formally designed system and a genuinely functioning Integrated Financial Crime Risk Management model. In regular processes, an organisation may appear stable: client due diligence is performed, transactions are monitored, policy requirements are followed and management reports are prepared. The true quality of control, however, becomes apparent when a signal deviates, a client fails to provide complete information, a transaction shows an unusual pattern, a sanctions hit requires further investigation, a tax structure is difficult to explain, an employee requests an exception or an incident may have reputational, legal or regulatory impact. At such moments, it must be clear how information moves through the organisation, who performs which assessment, when escalation is mandatory, which decision-making levels are involved and how records are kept. Without that understanding, there is a risk that signals remain unresolved, exceptions become normalised or incidents are treated as isolated events rather than symptoms of broader control weaknesses.

The movement of escalations through the first, second and third lines is often more complex in practice than policy documents suggest. The first line may identify a signal but hesitate as to whether it is sufficiently serious for formal escalation. The second line may request additional information, while depending on the completeness and quality of business input. Legal may become involved where contractual termination, liability, reporting obligations or sanctions law consequences are at stake. Tax may play a role where fiscal structures, substance, source of wealth or cross-border payments raise integrity questions. Audit may later assess whether the escalation process was consistent, timely and sufficiently substantiated. When this movement is not tightly designed, a vulnerable pattern emerges: risks are discussed informally, decisions are made orally, exceptions are insufficiently justified, follow-up is not monitored and lessons learned disappear once the file is closed. Integrated Financial Crime Risk Management must therefore treat escalations as critical control moments in which governance, substantive assessment, documentation and accountability come together.

For the client, a sharp understanding of escalations, exceptions and incidents is of significant value because it directly affects regulatory resilience, evidentiary quality and internal discipline. A regulator or auditor will not only want to see that an organisation has policies, but above all how the organisation responds when a risk presents itself concretely. The relevant questions are: was the signal identified in time, was the right expertise involved, was the risk analysis sufficiently substantive, was the decision proportionate, was any deviation from policy convincingly justified, was follow-up monitored, was management informed and were structural lessons translated into improvements to processes or controls? A strong Integrated Financial Crime Risk Management model makes these questions controllable in advance. Escalation is then not seen as an exception to the system, but as an essential part of the system. Exceptions are not treated as practical detours, but as explicit risk decisions. Incidents are not merely closed out, but used as a source for strengthening governance, policies, monitoring, training, data and assurance.

Focus on workable control rather than merely formal compliance

Workable control differs from merely formal compliance because it does not ask only whether rules exist, but whether they are genuinely executable, understandable, proportionate and effective in daily practice. In the Financial Crime domain, there is a constant temptation to seek comfort in extensive policy documents, detailed procedure manuals, large control matrices and formal attestations. Such elements are necessary, but they do not guarantee effective control. An organisation may have impressive documentation while simultaneously struggling with poor data quality, unclear role allocation, overly complex workflows, insufficiently trained employees, ineffective monitoring, impractical escalation criteria or controls that mainly require administrative effort. Integrated Financial Crime Risk Management therefore requires an approach in which formal compliance is connected to operational reality. The central question is not only whether an obligation has been correctly described, but whether it is performed at the right moment, by the right function, with the right information and with sufficient substantive sharpness.

Workable control requires regulation to be translated into processes that align with client journeys, transaction flows, systems, decision moments and responsibilities. Where, for example, a client acceptance process is overly dependent on manual exceptions, separate email coordination or interpretations by individual employees, control becomes vulnerable, even if the policy is substantively complete. Where transaction monitoring generates large numbers of alerts without adequate prioritisation, context or analytical capacity, the result is not stronger control but operational noise. Where escalation rules are so abstract that employees do not know when to act, the likelihood increases that relevant signals will be picked up too late or not at all. Workable control therefore means that Financial Crime controls are designed from the perspective of risk, usability, decision quality and evidentiary value. A control must not merely demonstrate that something has been done; it must contribute to a better decision, a sharper risk picture or a more effective intervention.

For the client, this focus offers practical and strategic added value. An Integrated Financial Crime Risk Management model that is too heavy, too formal or too detached from operations leads to delay, frustration, avoidance behaviour and reduced execution quality. A model that is workable, by contrast, increases the likelihood that employees will identify risks in time, apply policies correctly, avoid bypassing escalations and record files carefully. Workable control does not weaken compliance; it strengthens compliance because it narrows the gap between standard and execution. The legal and regulatory threshold remains fully relevant, but is translated into measures that can function within the organisation. The client thereby receives a control model that is not designed solely to look sound during testing, but to hold up in practice when risks arise, commercial pressure increases, information is incomplete or external questions must be answered convincingly.

A 360° view of governance, execution, monitoring and testing

A 360° view of governance, execution, monitoring and testing brings the full lifecycle of Financial Crime control into view. Governance determines who is responsible, what risk appetite applies, how decision-making takes place and which escalations require management attention. Execution determines how policies are applied in client due diligence, transaction processing, sanctions screening, tax assessment, contractual review, file-building and operational decision-making. Monitoring determines whether risk indicators are identified in time, whether controls function, whether trends become visible and whether management has relevant information. Testing determines whether the whole of design and operation is reliable, consistent and demonstrable. Integrated Financial Crime Risk Management can only be powerful when these elements are not assessed separately, but as an interdependent system. Weak governance undermines execution. Weak execution disrupts monitoring. Weak monitoring limits testing. Weak testing allows structural shortcomings to persist for too long.

In practice, many vulnerabilities arise because organisations are relatively strong in one area, while insufficiently managing the connection between the elements. An organisation may have a detailed governance structure, but insufficient visibility into actual first-line execution. It may have an extensive set of controls, but limited management information on effectiveness, backlogs, exceptions or recurring risk indicators. It may perform periodic monitoring, but insufficiently translate the outcomes into process improvement, training or policy adjustment. It may register audit findings, but fail to ensure sustainable remediation. A 360° view prevents such shortcomings from being assessed in isolation. The question is not limited to whether governance, execution, monitoring or testing is present, but focuses on the extent to which these elements feed one another. Does monitoring lead to better governance? Does audit lead to stronger execution? Does operational experience lead to better policy? Does incident analysis lead to sharper controls?

For the client, this creates a richer and more reliable picture of Financial Crime control. Integrated Financial Crime Risk Management becomes visible as a cyclical steering model in which policies, processes, controls, monitoring, escalation, reporting and testing are continuously connected. This offers concrete benefits: management decision-making is fed by better information, operational teams receive clearer frameworks, compliance can monitor in a more targeted way, legal and tax can be involved earlier in material risks, and audit can test themes that are genuinely relevant to risk and operation. A 360° view also makes visible where investments have the greatest impact. Sometimes the weakness is not a lack of additional policy, but data quality. Sometimes it is not more monitoring, but better prioritisation. Sometimes it is not additional training, but clearer escalation criteria. By analysing governance, execution, monitoring and testing in conjunction, an Integrated Financial Crime Risk Management model emerges that is sharper, more practical and more defensible.

Practice-driven integration as added value for Integrated Financial Crime Risk Management

Practice-driven integration forms the added value of Integrated Financial Crime Risk Management because it prevents integrity from being reduced to a formal framework that has insufficient grip on the reality in which risks arise. Financial Crime risks are dynamic, context-sensitive and often intertwined with commercial, legal, tax and operational factors. A theoretical model can provide direction, but only creates value when it is informed by practical experience: knowledge of client files, understanding of transaction flows, insight into system limitations, experience with regulatory questions, familiarity with audit findings, sensitivity to commercial pressure and understanding of how employees actually make decisions. Practice-driven integration means that Integrated Financial Crime Risk Management does not start from abstract ideals, but from the question of how control actually works, where it breaks down and how it can be strengthened in such a way that it has meaning in daily operations.

This approach requires a sharp eye for the difference between designed reality and lived reality. In designed reality, roles are clear, processes are logical, controls are effective, escalations are timely and files are complete. In lived reality, systems may not always provide the right information, employees may be confronted with unclear signals, commercial pressure may accelerate decisions, exceptions may be resolved pragmatically, compliance questions may be asked too late and audit findings may only reveal after the fact that the process was insufficiently robust. Practice-driven integration brings this gap to light without falling into mere criticism. The objective is not to increase complexity, but to make control more realistic. This is achieved by placing controls where risk arises, making decision criteria concrete, clarifying escalation channels, identifying data dependencies, sharpening governance and embedding evidentiary considerations from the outset of execution.

For the client, the added value lies in an approach that is strategically sharp and operationally applicable. Integrated Financial Crime Risk Management is not presented as an abstract compliance concept, but as a controllable system that helps make better decisions, reduce blind spots, strengthen accountability and increase regulatory resilience. Practice-driven integration makes visible which parts of the existing model can be retained, which parts must be revised and where simplification is possible without weakening risk management. The result is an approach in which legal standards, tax sensitivities, compliance requirements, business reality and audit expectations do not compete with one another, but are brought together into one coherent whole. The client thereby receives an Integrated Financial Crime Risk Management model that is not only substantively convincing, but also functions under the conditions in which Financial Crime risks actually present themselves.